The supply of natural gas to customers (distribution companies or end customers whose gas offtake at each supply point permanently amounts to a minimum of one million m3 per year) established in Belgium is subject to the prior granting of an individual permit issued by the Minister for Energy (except when it is carried out by a distribution company on its own distribution network).

The federal permit application dossiers are sent to the CREG which examines the criteria and then sends its opinion to the Minister for Energy.

In this context, the CREG gave ten positive opinions, following applications submitted by Lampiris,* Opinion (A)140130-CDC-1305 relating to an individual natural gas supply permit granted to Lampiris SA; Ministerial decree of 10 March 2014 (Official Journal of 20 March 2014). Eni gas & power,* Opinion (A)140206-CDC-1309 relating to an individual natural gas supply permit granted to Eni gas & power; Ministerial decree of 28 February 2014 (Official Journal of 18 March 2014). Electrabel Customer Solutions,* Opinion (A)140528-CDC-1324 relating to an individual natural gas supply permit granted to SA Electrabel Customer Solutions; Ministerial decree of 25 August 2014 (Official Journal of 15 September 2014). Electrabel,* Opinion (A)140619-CDC-1339 relating to an individual natural gas supply permit granted to SA Electrabel; Ministerial decree of 5 September 2014 (Official Journal of 19 September 2014). Eni,* Opinion (A)140710-CDC-1346 relating to an individual natural gas supply permit granted to Eni S.p.A. ; Ministerial decree of 18 July 2014 (Official Journal of 1 August 2014). E.On Global Commodities,* Opinion (A)140724-CDC-1356 relating to an individual natural gas supply permit granted to E.On Global Commodities SE; Ministerial decree of 25 August 2014 (Official Journal of 15 September 2014). Statoil,* Opinion (A)140918-CDC-1365 relating to an individual natural gas supply permit granted to Statoil ASA; Ministerial decree of 9 October 2014. Vattenfall Energy Trading Netherlands,* Opinion (A)141009-CDC-1376 relating to an individual natural gas supply permit granted to SA Vattenfall Energy Trading Netherlands; Ministerial decree of 9 December 2014 (Official Journal of 22 December 2014). GasTerra,* Opinion (A)141120-CDC-1387 relating to an individual natural gas supply permit granted to GasTerra BV; Ministerial decree of 30 December 2014 (Official Journal of 14 January 2015). and Wintershall Holding.* Opinion (A)141204-CDC-1389 relating to an individual natural gas supply permit granted to Wintershall Holding GmbH; Ministerial decree of 30 December 2014 (Official Journal of 14 January 2015). These applications and opinions have all resulted in the granting of ministerial decrees.

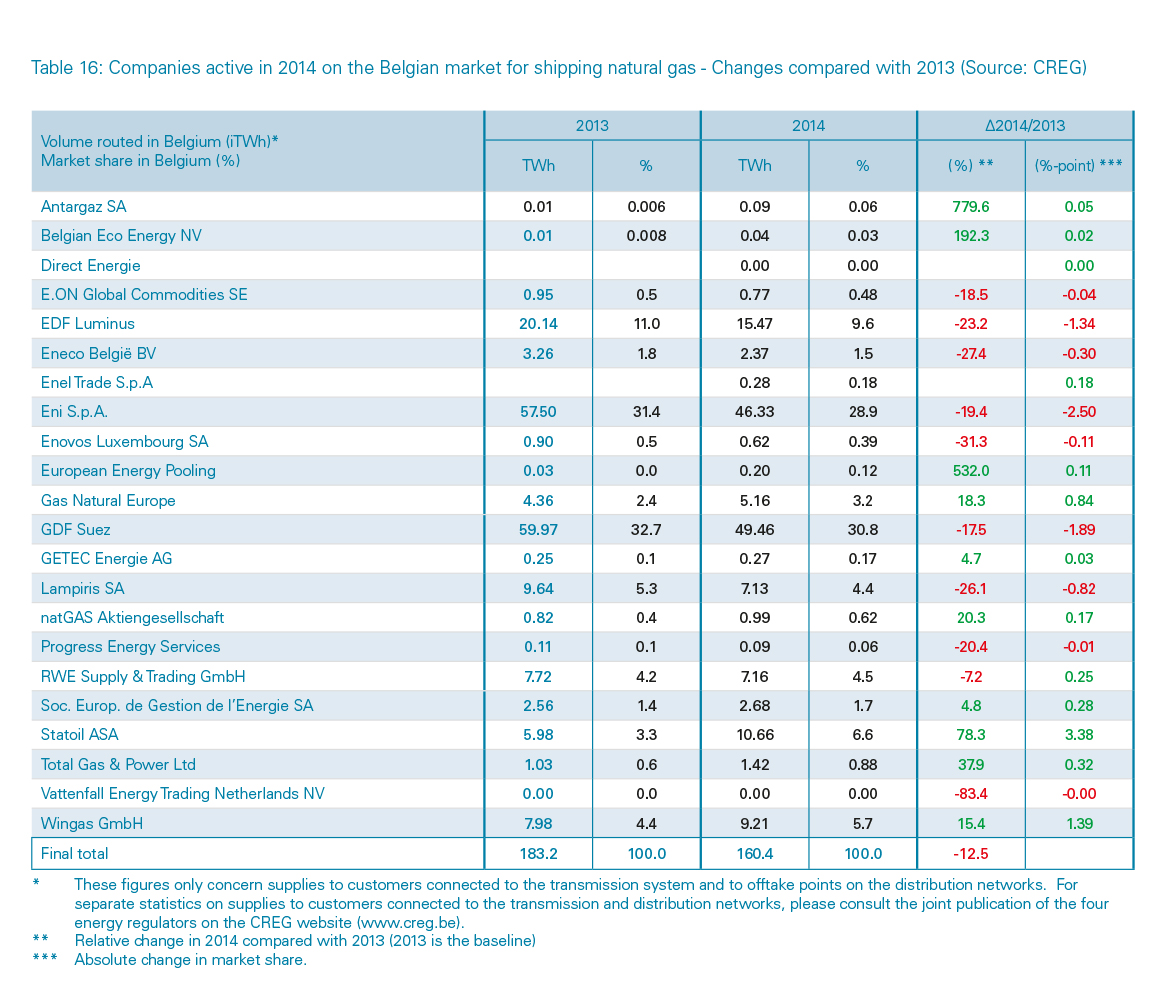

In 2014, total natural gas consumption* This evaluation is based on figures related to shipping activities as disclosed by the transmission system operator, such as they are communicated by the transmission system operator. amounted to 160.4 TWh, which represents a slight drop of 12.5% compared with consumption in 2013 (183.2 TWh). This decrease is the result of reduced consumption of natural gas in all consumer segments. We can observe a slightly lower consumption for end customers connected to the distribution networks (-18.7%), a sharp reduction in consumption for the generation of electricity (possibly combined with heat production) (-6.7%) and a limited reduction in consumption by industrial customers (-3.8%).

In 2014, two additional companies began to supply the wholesale market in natural gas: Direct Energie Belgium and Enel Trade S.p.A. If we include the takeover or integration of transmission operations in a business of the same group, twenty-two companies were active last year on the Belgian natural gas transmission market.

Although each of these companies has seen a decline in part of their market share, the top three supply companies have not changed in 2014, nor has their respective ranking. GDF Suez still occupies first place, with a market share of 30.8% (-1.9%). Eni is ranked in second place with 28.9% of the market share (-2.5%). EDF Luminus was not able to repeat its previous years’ successes during which it systematically benefited from limited growth: it lost 1.3% taking it to 9.6% of the market share.

Statoil, in fourth place, is the company which has seen the largest increase in 2014 by managing to almost double its market share, going up to 6.6%.

Wenger’s has seen an increase in volume of 1.4% in 2014, taking it to 5.7% of the market share.

For the first time in 2014, five companies had a market share greater than 5%. RWE Supply & Trading came sixth in the ranking, 4.5% (+0.3%). For the first time since joining the market, Lampiris has suffered a loss (-0.8%) and moves from 4th to 7th place in the rankings, under the threshold of 5% (4.4%). Gas Natural Fenosa has made progress once more (+0.8%), reaching 3.2% of the market share. SEGE (European Energy Management Company) increased its market share (+0.3%) to 1.7%. Furthermore, Eneco België obtained, despite a drop of 0.3%, a market share of 1.5% and, in doing so, becomes the final company to have a market share greater than 1%.

After Eni, the second biggest loser (-1.8%) is E.ON Global Commodities which saw its share of the market fall by almost a fifth from the previous year (0.5%).

Vattenfall Energy Trading Netherlands completely ceased its activities on the Belgian transmission network during 2013 and has disappeared from the market (-1.1% to 0.00%).

The other users of the active networks are Antargaz, Belgian Eco Energy, Direct Energie Belgium, E.ON Global Commodities, Enovos Luxembourg, Enel trade, European Energy Pooling, GETEC Energie, natGas, Progress Energy Services, Total Gas & Power and Vattenfall Energy Trading Netherlands. All of these companies each have a market share of less than 1%. Together, they hold 3% of the market share.

On 31 December 2014, thirty-five network users held a supply permit. Twenty-two of them conducted operations during 2014 on the transmission system for shipping natural gas to Belgian end customers. By way of comparison, at the end of 2007, just six network users were operating on the Fluxys Belgium transmission network for supplies to Belgian end customers.

Readers are referred to paragraph 3.1.2.2 of this report which applies mutatis mutandis to natural gas.

Readers are referred to paragraph 3.1.2.3 of this report, which also applies to natural gas.